The new 2018/19 tax year starting this April 2018 saw changes made to something known as the Dividend Tax Allowance. This taxable benefit allows an investor who receives dividends from shares to have a certain level of dividend income every tax year before tax has to be paid. If you are unfamiliar with the concept of dividends – they are simply payments that some companies pay to shareholders normally out of their profits.

So what is the change and why should you care?

In the tax year 2017/18 investors could earn £5000 tax free from dividends, but from 6/4/2018 the government reduced this to £2000. This could be quite a big deal if you are in the category of those affected below.

Who’s affected?

Employees or directors of small businesses paid partly or wholly via dividends instead of a salary

Anyone invested in direct company shares or a stocks and shares fund held outside a pension or ISA, earning dividends exceeding £2000. This roughly equates to £57000 or more in investments of income producing shares assuming a dividend rate of 3.5% per annum.

What’s the impact?

It means you have to pay tax on the amount over £2000 you receive from dividends depending on the tax bracket you sit in, as follows:

Basic rate taxpayers – 7.5%

Higher rate taxpayers – 32.5%

Additional rate taxpayers and trustees – 38.1%

In real numbers, this could mean you paying up to an extra £1143 tax a year depending on your tax status as shown below.

Basic rate taxpayer (£5000-£2000) x 7.5% = £225

Higher rate taxpayer (£5000 -£2000) x 32.5% = £975

Additional rate taxpayer (£5000 -£2000) x 38.1% = £1143

The reality is this: prior to April 2018, as an investor, you could have had about £143,000 invested in shares paying an average 3.5% annual dividend, and held them outside of an ISA or pension without worrying about paying any tax on the income. Post April 2018, that amount has now been reduced to roughly £57,000 (at 3.5% assumed annual dividend rate). That’s a lofty £86000 in dividend income (143000 – 57000) that could now be exposed to a tax charge.

The good news is there are ways you can avoid this new tax grab and shield the £86,000 of investments potentially exposed.

Here’s 5 simple suggestions, and don’t be put off by these industry terms if they are new to you.

Bed & ISA after 6th April 2018 (for the 2018/19 tax year)

Bed and ISA simply means selling some existing shares held outside of an ISA, and then immediately reinvesting the proceeds from the sale into the same or different shares inside an ISA (Individual Savings Account). This can be done simply using any online broking service provider. It is possible to invest up to £20000 in an ISA for the tax year 2018/19.

CAUTION: Be careful that any shares you sell when conducting the Bed and ISA process do not incur capital gains tax. Everyone has an annual allowance of £11,700 of capital gains that can be made in the tax year 2018/19 before capital gains tax is charged. It means being mindful and selective about the shares you sell if you want to avoid a potential capital gains tax charge.

Use your spouse’s ISA allowance

You can also use your spouse’s ISA allowance if your spouse has not taken full advantage of their annual allowance of £20,000. Using your spouse’s allowance for the tax year 2018/19 alongside your own means you can invest a total of £40,000 in ISA’s.

Bed & SIPP

Similar to Bed and ISA, but this time you sell your shares and immediately use the proceeds towards investing into shares within a SIPP. A SIPP stands for “Self-Invested Personal Pension”. By doing this, your shares are then protected inside the tax shelter of a pension, avoiding any future dividend or capital gains tax. It’s possible to invest a maximum of your total gross annual earnings into a SIPP up to the maximum of £40,000 for this tax year.

CAUTION: Only consider doing this if investing in a pension is relevant to your needs and investment goals. Review Step 6 of the masterMONEYsimply Journey Planner process if you are unsure.

Transfer into growth shares.

This is a strategy you could consider if you can’t use ISA’s and pensions to shelter your investments from tax, as long as you are happy moving away from income bearing shares and into shares that do not provide them. These type of shares are referred to as growth shares – they don’t provide dividends because the expectation is for the company and underlying share price to appreciate instead.

If the strategy suits your plans, then you could consider selling a suitable quantity of dividend bearing shares and buy into into growth shares, selling enough of them to take your annual dividend income to below the £2000 threshold.

You could also consider the possibility of using dividend producing shares for your ISA and pension parts of your investment portfolio, but growth shares outside of those vehicles. It’s then a case of managing your gains in order to make the most of your capital gains tax allowance every year.

CAUTION: Before doing this you should carefully consider whether this strategy is in line with your investment goals, your risk profile and the transaction costs.

As a summary, consider the following:

Costs of brokers fees buying and selling

Stamp duty costs when repurchasing shares

Risk profile differences between the income shares being sold and growth shares purchased

Does it fit your investment strategy (Step 6 of the masterMONEYsimply Journey Planner)

Junior Stocks and Shares ISA

This fifth option is more suitable if you are interested in the idea of gifting money to a child or a person you might be responsible for. This means it’s probably most appropriate if you are in the “fortunate” position to have concerns about a future inheritance tax liability. By doing this it can act as a way to reduce some of that liability.

Note that it’s possible to gift up to £3000 a year without any future inheritance tax liability, but you can invest more than that into the Junior Stocks and Shares ISA. The current limit for the tax year 2018/19 is £4260.

Summary

These 5 steps can help you to overcome the dividend tax allowance reduction, but remember, whenever making any investment decisions it is important to ensure it fits into your overall investment plans and goals. It is also well worth considering a review of your financial plans in their entirety, at least once a year.

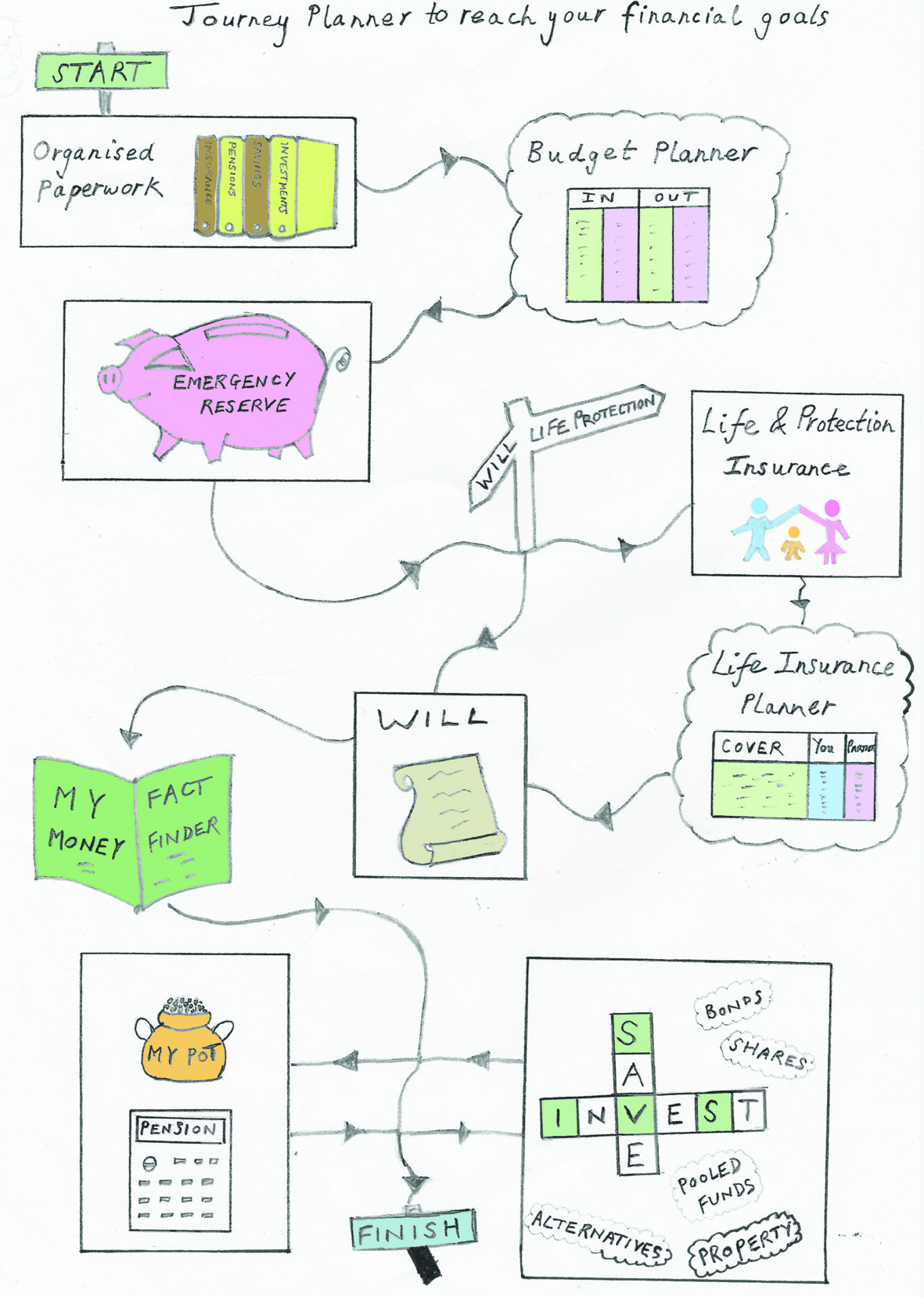

To help with your financial review, knowing where to begin and end, I have devised a Financial Journey Planner for anyone to easily follow. If offers a structured path for you to create your own tailor made financial plan. The idea is for you to do it yourself, simply, and hopefully avoid the pitfalls and normal costs and fees of achieving the result you want.

You can find out more about the Financial Journey Planner 8 steps and sign up to the masterMONEYsimply newsletter on our home page.

In addition I offer hourly fee based coaching to support and guide you through the Financial Journey Planner. Click here for more information.

DISCLAIMER:

Please note that the views expressed on this Website are personal opinions only. They should not be construed as financial advice. All information presented on the Website is intended for educational and informational purposes only, and not meant considered as financial advice. While all attempts are made to present accurate information, it may not be appropriate for your specific circumstances and information may become out-dated over time. The authors of the content on the Website are not finance experts, IFA’s, bankers, or legal professionals, and you should seek professional advice before making any financial decisions.

Please make sure to do your own due diligence and seek a trusted financial professional before making any financial decisions of your own.

No liability can be assumed for any technical, editorial, typographical or other errors or omissions within the information that is given.

{kind=link}